Retirement Savings: How Much Do You Need to Retire Comfortably?

Retirement savings are the accounts, investments, and cash reserves you set aside to help support your life after full-time work becomes optional. But saving for retirement is not only about building a large account balance. It is about knowing what you are saving for, how your money is invested, how taxes may affect your income, and how those assets can eventually support the life you want to live.

For many people, retirement begins with a 401(k), IRA, employer match, or investment account. Over time, those pieces need to work together. A strong strategy can help you understand how much to save, where to save it, how to invest it, and how your assets may one day become income.

At Strategic Investment Management, we help individuals and families in Austin and beyond approach retirement savings with purpose, vision, and direction. As an Austin-based fiduciary financial advisory firm, we help clients connect their retirement accounts, investment decisions, tax picture, insurance needs, and long-term goals into a coordinated plan.

Whether you are still building wealth, getting close to retirement, or already drawing income from your assets, the right guidance can help you make informed decisions with the money you have worked hard to build.

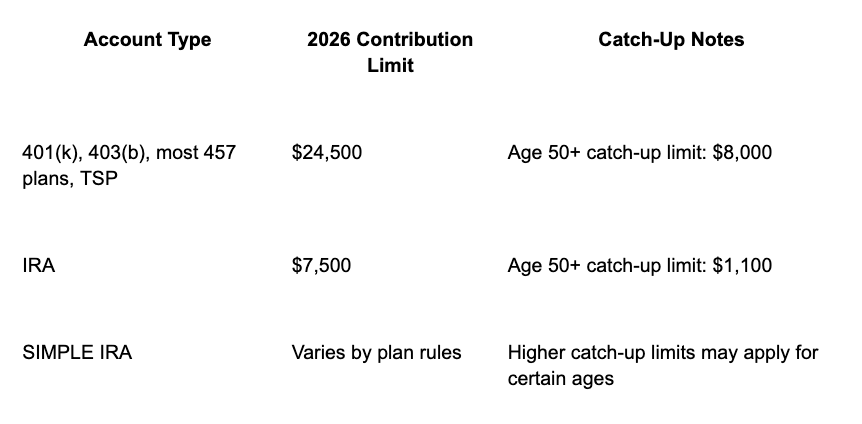

How Much Can You Contribute to Retirement Savings Accounts in 2026?

For 2026, the IRS increased several retirement savings contribution limits. Employees who participate in 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan can contribute up to $24,500. The IRA contribution limit increased to $7,500. The 401(k) catch-up contribution limit for those age 50 and older increased to $8,000, while the IRA catch-up contribution limit for those age 50 and older increased to $1,100.

These limits matter because they shape how much retirement savings you can direct into tax-advantaged accounts each year. However, the right contribution amount depends on your income, cash flow, tax situation, and overall financial plan.