Divorce can require you to sort through a shared financial life one account at a time. Retirement assets are often among the largest pieces to divide, and they come with specific rules, paperwork, tax treatment, and timing considerations.

Whether you are considering divorce, actively negotiating, or working through post-decree details, understanding how retirement accounts are divided can help you protect your share and make more confident decisions.

This guide explains how retirement assets are identified, valued, and divided; when a QDRO may be required; how IRAs are handled differently; and what tax and timing issues to watch before the process is complete.

Key Takeaways About Dividing Retirement Accounts in Divorce

Dividing retirement assets can be technical and emotional. Knowing the major rules before you begin may help reduce delays, avoid tax surprises, and protect your long-term financial stability.

Different accounts follow different rules. A 401(k), pension, traditional IRA, and Roth IRA are not divided the same way.

Only the marital portion is typically divided. Contributions and growth during the marriage are often considered marital property, while pre-marital balances may be separate.

Employer-sponsored plans may require a QDRO. A Qualified Domestic Relations Order tells the plan administrator how to divide benefits.

IRAs use a different process. Traditional and Roth IRAs are generally divided through a transfer incident to divorce, not a QDRO.

Taxes and timing matter. Incorrect withdrawals, vague language, or delayed paperwork can create unnecessary costs.

Documentation is essential. Statements, valuation dates, plan rules, and transfer confirmations should be carefully tracked.

What Retirement Assets Should You Identify First?

The first step is to create a complete inventory of retirement accounts. List each plan type, employer or custodian, account number, current balance, and ownership details.

Gather statements from key dates, including the date of marriage, separation date, filing date, or any other date used by the court to define the marital period. If older statements are missing, the plan administrator or custodian may be able to provide historical records.

Once the accounts are identified, the next step is determining what portion may be marital and what portion may be separate. Contributions and growth during the marriage are commonly treated as marital property. Pre-marital balances and their growth may be separate, depending on state law and available documentation.

This tracing process can become complicated, especially when accounts include rollovers, employer matches, loans, or years of market growth.

How Are 401(k)s, 403(b)s, and 457(b)s Divided?

Defined contribution plans, including 401(k), 403(b), and 457(b) accounts, usually have a clear account balance. In divorce, the division may assign a dollar amount or a percentage as of a specific valuation date.

Many orders also specify whether the alternate payee receives investment gains or losses from the valuation date through the transfer date. This detail matters because market movement can change the value before the transfer is completed.

For employer-sponsored retirement plans, the transfer typically requires a plan-approved domestic relations order. If the receiving spouse rolls the funds into an IRA or qualified employer plan, taxes are often deferred until future withdrawal, assuming the transfer is handled properly. Cash distributions, however, may create ordinary income tax and potential penalties.

How Are Traditional Pensions Divided in Divorce?

Traditional pensions are different because they promise future income rather than showing a simple account balance. A divorce order may assign a share of the future monthly benefit, often using a formula based on the years of service during the marriage.

Important pension decisions should be addressed early, including:

When benefits may begin

Whether the former spouse receives survivor benefits

How early retirement subsidies are handled

Whether cost-of-living adjustments apply

What happens if the employee spouse dies before retirement

Survivor benefits can be especially important. Without the right election and order language, payments may stop when the employee spouse dies.

What Is a QDRO and When Is One Needed?

A Qualified Domestic Relations Order, or QDRO, is a legal order used to divide certain employer-sponsored retirement plans in divorce. It instructs the plan administrator to pay a portion of the account or benefit to a former spouse.

QDROs commonly apply to 401(k)s, pensions, and other employer retirement plans governed by federal retirement law. IRAs do not use QDROs.

Each plan may have its own model language and approval process. When possible, submitting a draft QDRO to the plan administrator before court approval can help prevent delays, rejections, or expensive revisions later.

How Are Traditional and Roth IRAs Divided?

Traditional IRAs and Roth IRAs are divided through a transfer incident to divorce. This process does not require a QDRO, but it does require clear instructions in the divorce decree and careful coordination with the custodians.

The decree should identify the account, amount or percentage to transfer, and timeline for completion. Transfers should usually be handled directly between custodians, not by withdrawing funds personally and redepositing them.

For Roth IRAs, it is also important to preserve records tied to contribution basis and the five-year holding period. Proper documentation helps protect the account’s future tax treatment.

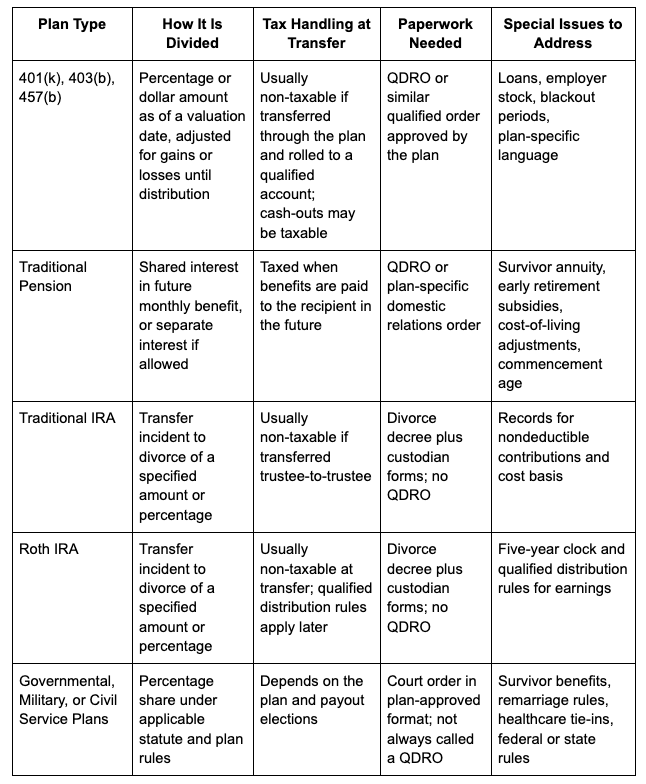

How Do Common Retirement Plans Compare in Divorce?

Why Do Valuation Dates and Market Movement Matter?

Every division order should define a valuation date. This is the date used to calculate the share being divided. Some couples use the separation date, filing date, divorce date, or a date close to distribution.

For daily-priced accounts, such as 401(k)s, the order may need to specify whether gains and losses apply between the valuation date and the transfer date. For pensions, valuation may require actuarial calculations.

Clear language can help reduce disputes and prevent one spouse from unintentionally bearing all market movement.

What Tax Issues Should You Watch?

Taxes depend on the type of retirement account and how the funds are transferred.

A QDRO transfer from a 401(k) to an IRA may preserve tax deferral. A cash payment from the plan, however, may be taxable as ordinary income. IRA transfers incident to divorce are generally not taxable at the time of transfer when handled properly, but later withdrawals remain subject to normal IRA rules.

Trustee-to-trustee transfers are often preferred because they may help preserve tax treatment and reduce reporting issues. Personal withdrawals can create avoidable taxes, penalties, or reporting complications.

What Mistakes Should You Avoid?

Dividing retirement assets can stall when orders are vague, paperwork is delayed, or plan rules are overlooked. Common mistakes include:

Waiting until after the divorce to draft plan orders

Using language the plan administrator will not accept

Forgetting to address gains and losses

Ignoring plan loans, employer stock, or blackout periods

Cashing out without understanding taxes

Failing to update beneficiary designations

Assuming the divorce decree automatically completes the transfer

Not confirming that funds were received by the correct account

A careful process can help reduce stress and protect both parties from avoidable errors.

What If the Divorce Is Final but the Transfer Never Happened?

If a divorce decree addressed a retirement account but the transfer was never completed, contact the plan administrator or QDRO department for next steps. In many cases, a court may still issue a post-divorce domestic relations order to enforce the original agreement.

If the decree did not mention a retirement account that existed during the marriage, speak with an attorney about available options. Timing, state law, and documentation will all matter.

Who Should Help Coordinate the Process?

Dividing retirement accounts is both a legal and financial process. Each professional has a different role.

Your attorney drafts and reviews the legal language. The plan administrator confirms what the plan will accept. A QDRO specialist may help prepare plan-specific orders. Your financial advisor can help you understand values, tax treatment, rollover options, and how the divided assets fit into your long-term financial plan.

Strong coordination can help reduce confusion during an already difficult transition.

Retirement Asset Division Checklist

Use this checklist to stay organized:

Gather current and historical plan statements.

Confirm the marital period and valuation date.

Identify each account type and plan administrator.

Decide whether the division is by percentage or dollar amount.

Address gains, losses, loans, survivor benefits, and special plan features.

Request plan model language when available.

Submit draft orders for pre-approval when possible.

Coordinate trustee-to-trustee transfers.

Confirm that each transfer was completed.

Update beneficiary designations after the divorce.

Frequently Asked Questions About Dividing Retirement Accounts in Divorce

What is the marital portion of a retirement account?

The marital portion generally includes contributions and growth earned during the marriage. Pre-marital balances may remain separate, depending on state law and available records.

Do we divide retirement accounts by dollar amount or percentage?

Percentages are often safer because they can adjust for market movement between the valuation date and transfer date. A fixed dollar amount may be appropriate in some cases, but it should be clearly documented.

Do all retirement accounts require a QDRO?

No. QDROs are generally used for employer-sponsored plans such as 401(k)s and pensions. IRAs and Roth IRAs are usually divided through a transfer incident to divorce.

Will I owe taxes when I receive my share?

If the transfer is handled correctly through a QDRO or transfer incident to divorce, the transfer itself may not be taxable. Cashing out funds is usually taxable and may trigger penalties.

How long does a QDRO take?

Timelines vary by plan, but many administrators take several weeks, often around 4–8 weeks, to review and approve an order once submitted. Submitting a draft early can help avoid delays.

Can retirement assets be offset against other property?

Yes, but after-tax value matters. A pre-tax retirement account is not the same as a taxable brokerage account, home equity, or cash. Professional valuation may help compare assets fairly.

Can a QDRO be issued after divorce?

Yes, post-divorce QDROs are often used to enforce prior agreements. Acting quickly can help reduce administrative complications.

Guidance for Dividing Retirement Assets

Retirement accounts represent years of saving, planning, and sacrifice. During divorce, handling them carefully can help protect your financial stability and your ability to move into and throughout retirement with confidence.

Following a methodical process can help. Steps for dividing retirement assets may include:

Identifying the accounts

Determining the marital portion

Choosing the right order or transfer method

Understanding the tax treatment

Verifying completion

At Strategic Investment Management in Austin, TX, we help clients navigate complex financial transitions with clarity and coordination. If you are going through divorce and want to understand how retirement assets may fit into your broader financial plan, our team can help you evaluate your options and prepare for the road ahead.