Retirement planning looks different when a privately held business is one of your largest assets. The question is not only whether you have enough to retire, but how to turn years of ownership into flexible, tax-aware liquidity.

For many owners, stepping back does not mean walking away overnight. It means choosing an exit path that fits your timeline, financial needs, leadership team, family dynamics, and goals for the next chapter.

This guide covers common business exit strategies, how to prepare your company before a transition, what to consider around valuation and deal structure, and how to connect the sale or succession plan with your retirement income strategy.

Key Takeaways for Business Owners Nearing Retirement

The right exit strategy depends on your priorities: liquidity, control, legacy, cultural continuity, family involvement, or future upside.

Preparation often matters as much as the buyer. Cleaner financials, documented processes, and reduced owner dependence can support a stronger transition.

Deal structure and taxes may have a greater impact on your real outcome than headline valuation.

A business exit should be coordinated with retirement income planning, estate planning, and your personal vision for life after ownership.

What Business Exit Strategy Fits Your Retirement Goals?

Every exit route affects liquidity, control, complexity, and continuity differently. Before choosing a path, clarify what matters most: a clean break, ongoing income, family legacy, employee stability, or the opportunity to remain involved in a limited role.

1. Selling to an External Buyer

An outright sale to a strategic or financial buyer may offer meaningful liquidity and a defined transition timeline. Strategic buyers may value market fit, customer relationships, or operational synergies. Financial buyers often focus on cash flow, growth potential, and scalability.

This path can be attractive if you want to reduce day-to-day involvement, but many deals include seller notes, earn-outs, or rollover equity. The business also needs to stand on its own without relying heavily on your personal relationships.

2. Management Buyout

A management buyout allows an existing leadership team to purchase the business. This can preserve culture, client relationships, and institutional knowledge. Financing often includes a mix of bank debt, buyer equity, and seller financing.

For owners who want to taper involvement without remaining responsible indefinitely, an MBO can be a practical middle ground.

3. Employee Stock Ownership Plan

An ESOP allows a qualified retirement plan to purchase some or all company stock for employees. It can support employee retention and, in certain cases, create tax advantages. However, ESOPs require feasibility work, independent valuation, ongoing administration, and stable cash flow.

This path is usually best suited for companies committed to broad-based ownership and long-term continuity.

4. Family Succession

Family succession can protect legacy and preserve continuity, but it requires clear governance. Roles, compensation, voting rights, ownership percentages, buy-sell terms, and expectations should be documented early.

This is especially important when some heirs work in the business and others do not. A thoughtful structure can help reduce ambiguity and protect family relationships.

5. Recapitalization

A recapitalization allows you to take partial liquidity while bringing in a capital partner. This can help diversify your wealth while keeping some ownership and future upside.

The trade-off is that control may shift depending on the terms, investor rights, and growth plan.

6. Orderly Wind-Down

If a sale is not practical or the business is highly owner-dependent, an orderly wind-down may be the most responsible option. The focus becomes fulfilling obligations, serving clients well, monetizing assets, reducing risk, and closing with intention.

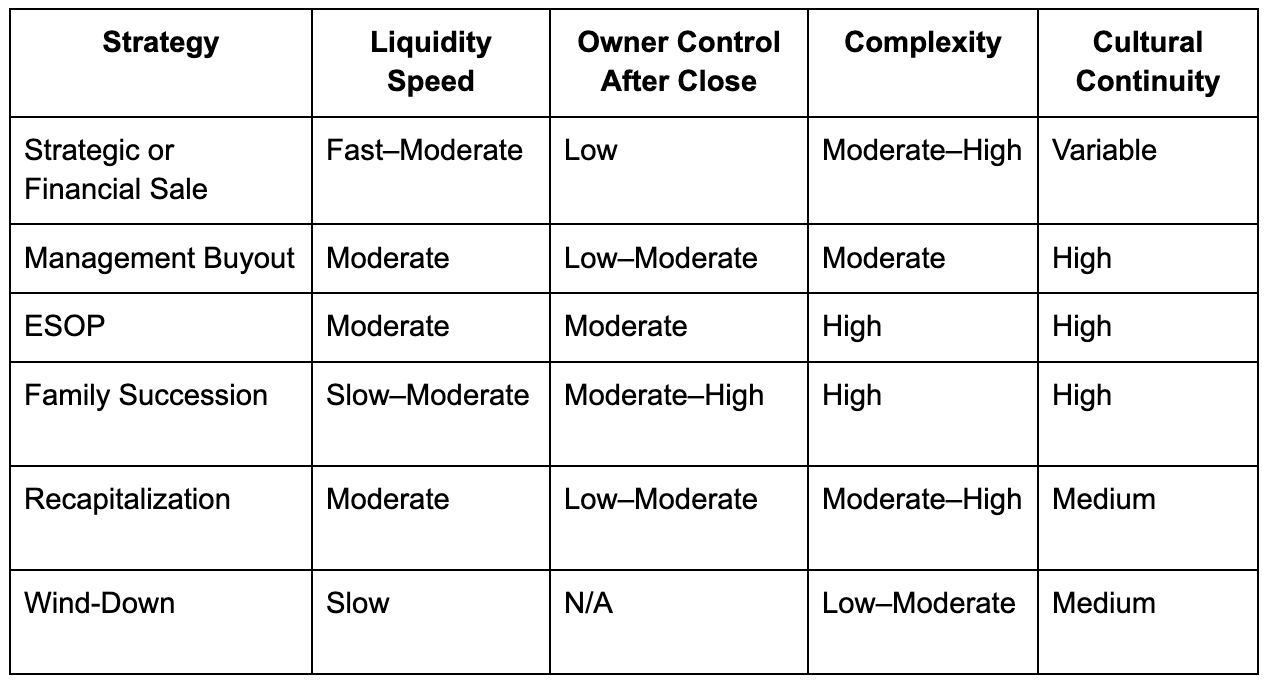

How Do Common Exit Strategies Compare?

No single column tells the full story. The best exit strategy is the one that aligns your financial needs, retirement timeline, risk tolerance, and goals for the company’s future.

How Can Owners Prepare a Business for Exit?

Buyers and successors typically value transferable cash flow. That means preparation should focus on making the business less dependent on you and more attractive to the next leader or owner.

Start by strengthening these areas:

Financial clarity: Maintain clean, organized financial statements that clearly show revenue, expenses, add-backs, and working-capital trends.

Lower key-person risk: Document processes, cross-train employees, and reduce reliance on your personal relationships.

Customer diversification: Heavy revenue concentration with one client can reduce value or create tougher deal terms.

Contract readiness: Review customer, vendor, employment, and lease agreements for transferability and renewal terms.

IP and compliance: Confirm intellectual property ownership, licensing, cybersecurity controls, privacy standards, and regulatory requirements.

Corporate records: Keep ownership records, board minutes, entity documents, and legal files current.

Many owners begin this work 18 to 36 months before a planned transition. Early preparation can create more choices and reduce pressure when negotiations begin.

Why Do Valuation, Deal Terms, and Taxes Matter So Much?

A high headline price does not always mean a better outcome. What matters is the after-tax amount you receive, when you receive it, how much risk you retain, and how involved you must remain after closing.

Valuation is typically a range, not a fixed number. It depends on earnings quality, growth prospects, risk, buyer competition, and industry conditions. A third-party valuation or quality-of-earnings review can help set expectations before going to market.

Deal structure may include:

Up-front cash

Seller financing

Earn-outs tied to future performance

Escrows or holdbacks

Rollover equity

Consulting or transition agreements

Tax planning should begin early. Entity type, asset versus stock sale treatment, state tax rules, installment sale options, and pre-transaction cleanup can all affect net proceeds. Coordinating with a CPA, transaction attorney, and financial advisor can help you understand how the deal supports your retirement income needs.

How Does a Business Sale Become Retirement Income?

The transaction is only one chapter. The next step is converting proceeds from a concentrated business asset into a retirement income plan.

A written plan can help you evaluate:

How much you need after taxes to support your lifestyle

How inflation, health care, and market volatility could affect income

Whether to invest proceeds all at once or in phases

How Social Security, Medicare, pensions, or required minimum distributions fit in

How estate planning and beneficiary designations should be updated

This is also an emotional transition. Many owners underestimate the shift from operator to retiree, investor, mentor, board member, philanthropist, or consultant. Planning your time can be just as important as planning your portfolio.

What Timeline Should Owners Follow Before Exiting?

A simple timeline can help organize the work:

- 0–6 months: Clarify personal goals, income needs, preferred exit paths, and advisory team. Begin a readiness assessment.

- 6–18 months: Clean up financials, document processes, reduce concentration risks, update contracts, and explore MBO, ESOP, or buyer options.

- 18–36 months: Launch a sale or succession process once business readiness and personal planning are aligned. Coordinate tax-aware strategies and finalize a post-exit income plan.

The timeline can flex, but sequencing matters. Business planning and personal planning should move together.

Frequently Asked Questions About Business Exit Strategies

How do earn-outs work?

Earn-outs tie part of the sale price to future performance. They can increase total proceeds if targets are met, but the terms should clearly define metrics, timelines, measurement methods, and decision rights.

Is an ESOP too complicated for a smaller company?

Not always. ESOPs require cost, oversight, and administration, but they may work for smaller companies with stable cash flow, strong leadership, and a culture suited to employee ownership.

What if my children are not aligned on taking over?

Use a structured governance process. Define roles, compensation, voting rights, ownership expectations, dispute resolution, and buy-sell terms. In some cases, trust planning may help separate economic benefits from management control.

Should I create my retirement investment plan before or after the sale?

Ideally, before. A pre-sale investment policy can help prevent rushed decisions after closing and connect expected after-tax proceeds to your income, risk, and legacy goals.

What happens if a deal falls through?

Maintain operational momentum and keep alternative paths open. A failed deal does not have to derail retirement if you have considered options such as an MBO, recapitalization, delayed sale, or wind-down.

Exit Planning Is a Process

A successful exit is not just about finding a buyer. It is about aligning your business readiness, deal terms, tax strategy, retirement income plan, and personal vision for what comes next.

At Strategic Investment Management, we help business owners approach major financial transitions with clarity, coordination, and confidence. If you are thinking about stepping back from your business, our team can help you evaluate how a potential exit may fit into your retirement income, investment, and legacy planning.

Ready to plan your next chapter? Contact Strategic Investment Management to start a conversation about your business exit strategy and retirement goals.